Pension Credit: The Free Government Top-Up Worth Up to £8,400 a Year That Millions of Retirees Simply Never Claim

Around 880,000 eligible UK pensioners are not claiming Pension Credit — leaving an estimated £1.7 billion in government support untouched every year. The average unclaimed entitlement is worth up to £8,400 annually. This is not a niche loophole; it is a mainstream benefit that the system has quietly failed to distribute.

The 0% Credit Card Cash Flow Strategy: How Disciplined UK Investors Are Using Balance Transfer Windows to Fund Their ISA Before April's Deadline

With the ISA deadline on 5 April 2026 now days away, a growing cohort of financially literate UK households is deploying an unconventional tactic: using 0% balance transfer and purchase credit cards to free up cash flow, then redirecting that liquidity directly into Stocks and Shares ISAs or high-interest Cash ISAs. The maths can work — but only for those who understand exactly where the strategy breaks down.

The £3,900 Pension Credit Ghost: Why 850,000 Eligible Pensioners Are Leaving Free Money on the Table Every Single Year

Pension Credit is one of the most valuable benefits available to low-income retirees in the UK, yet nearly one million eligible pensioners are not claiming it. Beyond the headline £3,900 annual gain lies a cascade of additional entitlements — from free TV licences to council tax reductions — that push the true annual value considerably higher.

The 0% Debt Mirage: How Britain's Most Trusted Credit Card Tool Is Quietly Backfiring for 1.2 Million Borrowers

Balance transfer credit cards have long been promoted as the definitive solution to expensive credit card debt. But for 1.2 million UK cardholders, the mechanics of these deals are creating new financial problems — from hard credit searches that damage mortgage applications to revert rates that can exceed 25% APR the moment the promotional window closes.

The 13.8% Pay Rise Your Employer Is Keeping: How 3.4 Million UK Workers Can Reclaim Hidden Pension Savings Before the Tax Year Ends

Salary sacrifice pension contributions generate a National Insurance saving worth 13.8% of every pound redirected — but millions of UK workers never see this money because their employer retains it. With the new tax year beginning 6 April 2026, there is a narrow window to negotiate before contribution rates reset and the opportunity closes for another twelve months.

Why the 4% Rule Does Not Work for British Investors — and the Revised Number You Should Be Using Instead

The 4% safe withdrawal rule was built on American market data, American inflation history, and American retirement structures. British investors who apply it uncritically are using a tool calibrated for the wrong conditions. Here is the UK-specific research on sustainable withdrawal rates — and the revised figure that actually reflects British market history, gilt yields, and the State Pension.

Déjà Vu Portfolio: How Millions of UK ISA Holders Are Tripling Down on the Same Ten Stocks Without Knowing It

Holding a Vanguard LifeStrategy, an HSBC World Index, and a Fidelity fund simultaneously feels like diversification — but for 3.2 million UK investors, it is anything but. Beneath the surface, these popular funds share an alarming concentration in the same handful of US mega-cap technology stocks. Here is how to check your own portfolio and what genuine diversification actually looks like in 2026.

The Five-Year Retirement Gamble: Why Drawing Your ISA at 55 Could Leave You £34,000 Worse Off Than Waiting Until 60

The FIRE movement has convinced a growing number of UK millennials that their Stocks and Shares ISA can fund retirement at 55. The maths of compound growth supports the dream — but the maths of sequence-of-returns risk tells a very different story. Withdrawing five years too early, in the wrong market conditions, could permanently reduce your retirement income by £34,000 or more.

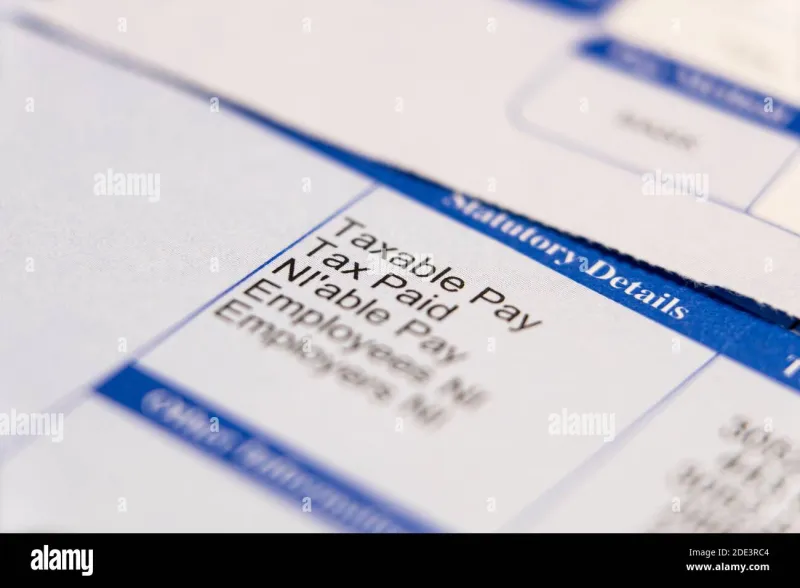

The £2,800 Pay Rise Penalty: How Frozen NI Thresholds Are Punishing UK Workers at Specific Salary Points — and the Legal Workaround That Eliminates the Problem

In 2026, frozen National Insurance and income tax thresholds have created salary points where a small pay increase produces a net-negative outcome after deductions. Workers earning near these cliff edges can legally eliminate the problem through pension salary sacrifice — but fewer than one in five eligible employees currently does so.

Forgotten Fortunes: How 1.2 Million UK Investors Are Silently Losing Money Across ISAs They No Longer Remember Opening

Platform mergers, workplace auto-enrolment schemes, and forgotten login credentials have left more than a million UK savers running fragmented portfolios they have completely lost track of. The cost of that fragmentation is measurable — and the April 2026 ISA deadline makes consolidation more urgent than ever.

Mortgage or Savings? The £3,600 Annual Miscalculation That UK Homeowners Keep Making When Their Fixed Rate Ends

When a fixed-rate mortgage expires, millions of UK homeowners instinctively reach for the overpayment option. In the current rate environment, that instinct is costing many of them more than £3,600 a year. Three modelled scenarios show why the maths is more nuanced than the default assumption suggests.

The £43,000 Couples Tax Trap: Why Joint Retirement Planning Is Quietly Destroying Your Pension Wealth

Most UK couples plan retirement as one financial unit, but HMRC treats you as two separate taxpayers. This mismatch creates a hidden tax liability that costs dual-pension households an average of £43,000 over retirement.

The £127,000 Overpayment Error: Why Your Mortgage Shouldn't Be Your First Debt Priority in 2026

Millions of UK homeowners are rushing to overpay mortgages at 5.2% while ignoring credit card debt at 24.9% and missing ISA returns at 7.8%. The maths reveals a costly emotional decision that's quietly destroying household wealth.

The Great British Money Hunt: £340 Billion in Lost Assets Could Include Yours — Here's How to Track Them Down

Millions of UK adults are sitting on forgotten financial assets worth thousands — from dormant bank accounts to lost pension pots. With the new tax year approaching, now's the perfect time to conduct your own financial treasure hunt.

The £586 Annual Payroll Error: Why Most UK Workers Are Using the Wrong Pension Contribution Method

Salary sacrifice pension contributions save higher-rate taxpayers up to £586 annually compared to relief-at-source, yet 67% of UK schemes default to the less efficient method. Here's how to check and switch.

The £127,000 Regional Reality Check: Why Your Retirement Pot Size Should Depend on Your Postcode

ONS data reveals a £200,000 pension pot lasts 14 years in rural Wales but only 8 years in London. Here's how to calculate what you actually need based on where you plan to retire.

The Notice Period Nightmare: Why 30-Day Savings Accounts Are Trapping UK Savers at the Worst Possible Moments

Notice accounts offer marginally higher rates but lock away funds when you need them most. Analysis of Atom Bank, Investec, and Aldermore shows the real cost of illiquidity during market downturns.

The £127,000 Inheritance Gap: Why Your ISA Beneficiary Nomination Is Probably Wrong — Or Missing Entirely

Unlike pensions, ISAs don't automatically bypass inheritance tax or probate. Millions of UK investors have outdated or missing beneficiary nominations, creating costly legal complications their families will inherit.

The Portfolio X-Ray: What 6.2 Million UK Investors Don't Know About Their ISA Holdings Could Cost Them Thousands

Most UK investors pour money into ISA tracker funds without ever examining what they actually own. Our investigation reveals dangerous concentration risks and hidden overlaps that could derail retirement plans.