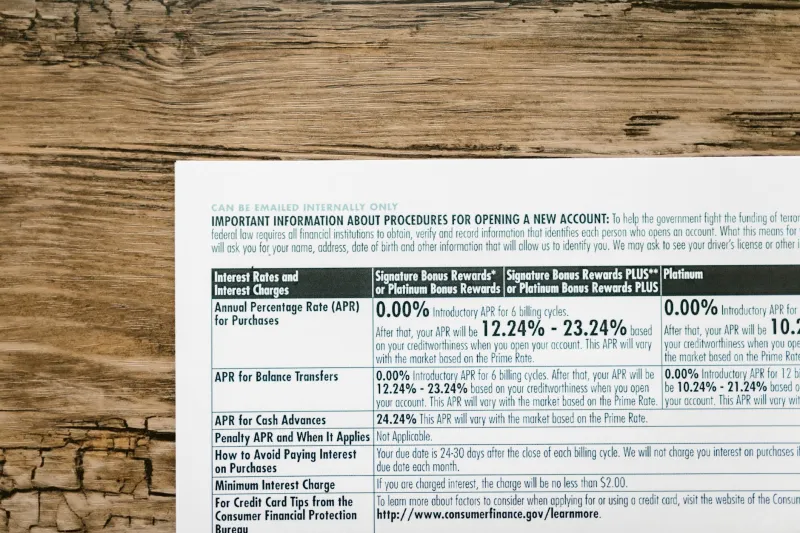

The Staggering Scale of UK's Sleeping Money Crisis

A shocking £47 billion sits idle in UK current accounts, earning virtually nothing while easy-access savings rates hover above 5%. For the average household with £10,000 in their current account, this represents a staggering £500 annual loss in potential interest — money that could be earned with zero additional risk and minimal effort.

The numbers are stark. While the Bank of England base rate remains at 5.25%, major high street banks continue paying 0.01% to 0.25% on current account balances above their monthly credit interest thresholds. Meanwhile, top-tier easy-access savings accounts are offering 5.1% to 5.25% — a differential that costs UK households collectively £2.35 billion annually in foregone interest.

Photo: Bank of England, via c8.alamy.com

Photo: Bank of England, via c8.alamy.com

The Real Cost: What You're Actually Losing

Let's quantify the damage with real numbers:

- £5,000 current account balance: Earning £1.25 annually at 0.025% vs £255 in a 5.1% easy-access account = £254 annual loss

- £10,000 current account balance: Earning £2.50 annually vs £510 = £508 annual loss

- £20,000 current account balance: Earning £5 annually vs £1,020 = £1,015 annual loss

These calculations assume you maintain a £1,000-£2,000 buffer in your current account for daily expenses — the rest should be working harder.

Your Step-by-Step Money Recovery Plan

Step 1: Same-Day Savings Switch (Complete Today)

Best Easy-Access Rates Available Now:

- Trading 212 Cash ISA: 5.2% (ISA-eligible, instant access)

- Marcus by Goldman Sachs: 5.1% (non-ISA, instant access)

- Chase Saver: 5.1% (existing Chase customers, instant access)

- Atom Bank Instant Saver: 5.05% (app-based, instant access)

Photo: Goldman Sachs, via media.skydb.net

Photo: Goldman Sachs, via media.skydb.net

Action: Open one of these accounts online today. Most providers offer same-day setup with instant bank transfers up to £25,000.

Step 2: ISA Deadline Sprint (Complete by 5 April 2026)

With just days remaining before the 2025-26 ISA year ends, prioritise tax-free savings:

Cash ISA Options:

- Trading 212 Cash ISA: 5.2% (no minimum, instant access)

- Chip Cash ISA: 5.15% (app-based, £1 minimum)

- Monzo Cash ISA: 5.1% (existing customers, instant access)

Maximum Impact: If you haven't used your £20,000 ISA allowance, moving this amount from a 0.01% current account to a 5.2% Cash ISA generates £1,040 additional annual interest — completely tax-free.

Step 3: The Current Account Audit

Keep in Your Current Account:

- Monthly expenses (rent, bills, groceries)

- Emergency buffer (£1,000-£2,000)

- Direct debit buffer (£500-£1,000)

Move to High-Interest Savings:

- Everything else above this operational minimum

- Irregular expenses fund (holidays, car repairs)

- Short-term savings goals

Platform-Specific Instructions

For Marcus by Goldman Sachs Users

- Apply online at marcus.co.uk

- Verification typically takes 24-48 hours

- Initial deposit minimum: £1

- Maximum balance: £250,000

- Withdrawals: Same-day via faster payments

For Trading 212 Cash ISA Users

- Download Trading 212 app

- Complete ISA application (5-10 minutes)

- Fund via bank transfer (instant)

- 5.2% rate applied immediately

- No fees, no minimum balance

For Chase Saver Users

- Existing Chase current account required

- Set up through Chase app

- Instant access to funds

- Rate linked to Bank of England base rate

The ISA Transfer Opportunity

If you already hold Cash ISAs with poor rates, initiate transfers immediately:

Current Poor Performers:

- HSBC Cash ISA: 1.5%

- Barclays Cash ISA: 1.8%

- Lloyds Cash ISA: 2.1%

Transfer Process:

- Open new Cash ISA with target provider

- Request ISA transfer (not withdrawal)

- Transfer typically completes within 15 working days

- Maintain tax-free status throughout

What to Watch in the Next 30 Days

Rate Movement Indicators:

- Bank of England MPC meeting (6 February 2026)

- Inflation data release (19 February 2026)

- US Federal Reserve policy announcement (1-2 February 2026)

Savings Rate Trends: Easy-access rates have held steady above 5% for three consecutive months. However, fixed-rate bonds (12-month terms) are offering 5.4% to 5.6%, suggesting providers expect rates to fall later in 2026.

Strategic Timing: Complete your ISA allocation before 5 April 2026, but consider fixing a portion of non-ISA savings for 12 months if you won't need immediate access.

The Bottom Line

Moving £10,000 from a typical current account earning 0.01% to a 5.2% easy-access savings account takes less than 30 minutes online and generates an additional £520 annually — equivalent to a 5.2% pay rise on that money. With the ISA deadline approaching, there's no financial excuse for leaving substantial sums in current accounts earning virtually nothing.

Your immediate action plan: Transfer excess current account funds to a 5%+ savings account today, maximise your remaining ISA allowance before 5 April, and set a monthly reminder to review rates quarterly.

This isn't about investment risk or complex financial products — it's about claiming free money that's already yours.

This article is for informational purposes only and does not constitute financial advice. Your capital is at risk. Past performance is not a reliable indicator of future results.